When a roof reaches the end of its service life or suffers sudden damage, filing a roof replacement insurance claim is often the most cost‑effective way to restore your home without draining your savings. Homeowners who act quickly, document damage thoroughly, and understand the insurer’s expectations can secure a settlement that covers a full replacement, including any necessary upgrades to meet current energy‑efficiency standards.

Understanding Roof Replacement Insurance Claims

Insurance policies typically differentiate between “repair” and “replacement” coverage. A replacement claim reimburses the cost of installing a new roof that matches the original in material, style, and performance, while repair coverage only addresses the specific damaged area. Most standard homeowners’ policies, such as those offered by State Farm and Allstate, include coverage for sudden, accidental damage (e.g., hail, wind, or fire) but exclude wear‑and‑tear or gradual deterioration.

According to the Insurance Information Institute’s 2026 report, roof‑related claims accounted for 18 % of all homeowner claim dollars, with storm damage leading the charge. Understanding whether your loss falls under an “all‑perils” or “named‑perils” policy is the first step in determining eligibility.

Table of Contents

- Understanding Roof Replacement Insurance Claims

- Key Documentation and Evidence

- Step‑by‑Step Process for Filing a Roof Replacement Insurance Claim

- 1. Immediate Safety Measures and Temporary Repairs

- 2. Contacting Your Insurer Promptly

- 3. Preparing a Detailed Claim Package

- 4. Navigating the Adjuster Inspection

- 5. Negotiating Settlement and Choosing a Contractor

- Common Pitfalls and How to Avoid Them

- Impact of Roofing Materials and Siding on Claim Valuation

- Case Study: A 2026 Hailstorm in the Midwest

- FAQ – Frequently Asked Questions

- What is the typical deductible for a roof replacement claim?

- Can I claim for roof decking and underlayment?

- Do insurance policies cover roof upgrades for better energy efficiency?

- How long does the claim process usually take?

- What if the insurer denies my claim?

- Final Thoughts

Key Documentation and Evidence

Insurers rely heavily on concrete evidence to assess the scope of loss. The following items form the backbone of a strong claim package:

- High‑resolution photographs taken from multiple angles, both before and after the incident. Include close‑ups of torn shingles, water stains on interior ceilings, and any surrounding siding damage.

- Professional roof inspection reports from a licensed roofing contractor. These reports should detail the extent of damage, identify the cause (e.g., hail impact versus water intrusion), and provide a written recommendation for full replacement.

- Itemized estimates that break down labor, materials, disposal fees, and any additional costs such as permits or scaffolding. Compare at least two estimates to demonstrate market‑rate pricing.

- Proof of ownership and policy documents, including the declaration page that lists coverage limits and deductible amounts.

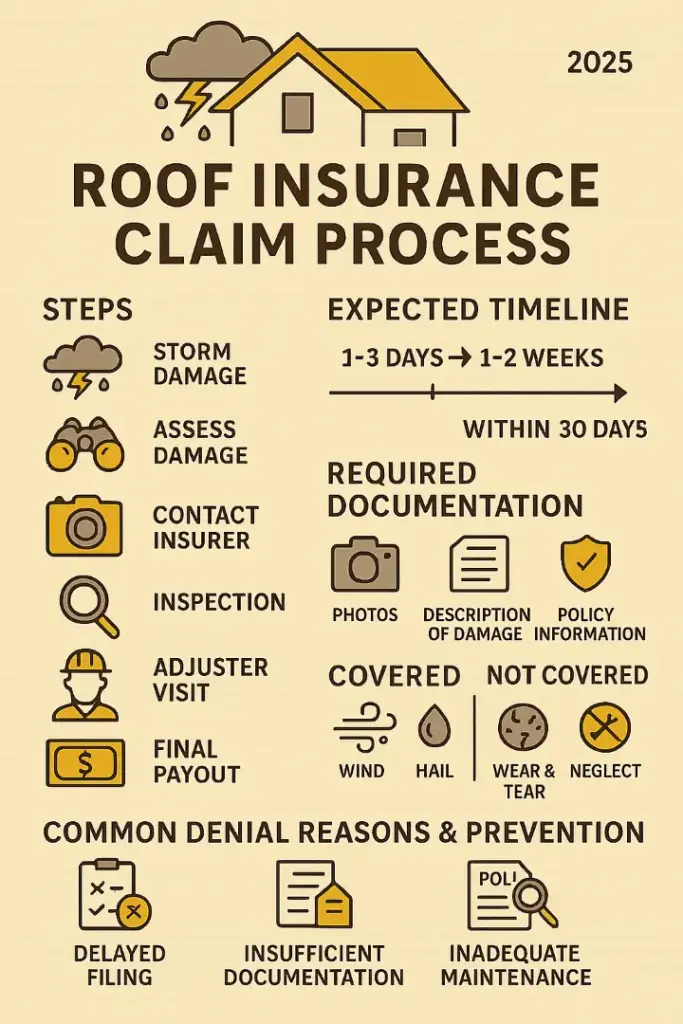

Step‑by‑Step Process for Filing a Roof Replacement Insurance Claim

1. Immediate Safety Measures and Temporary Repairs

Before you contact the insurer, ensure the property is safe. If a portion of the roof has collapsed, install a temporary tarp or a professional “temporary roof patch” to prevent further water ingress. Many policies require that you mitigate additional damage, and failure to do so can result in a reduced settlement.

2. Contacting Your Insurer Promptly

Most carriers set a 24‑hour window for reporting sudden loss. Call the claims hotline, provide the date of the incident, and request a claim number. During this call, ask for the name of the assigned insurance adjuster and inquire about the documentation checklist.

3. Preparing a Detailed Claim Package

Compile the evidence listed above into a single PDF folder. Include a concise cover letter that outlines:

- The cause of loss (e.g., “hail storm on 03/12/2026”)

- The date you first noticed the damage

- Actions taken to secure the property

- A request for full roof replacement under the policy’s replacement‑cost endorsement.

Attach the roof inspection report, photos, and at least two contractor estimates. If your home features energy‑efficient roofing or upgraded siding, add product specifications to demonstrate added value.

4. Navigating the Adjuster Inspection

When the insurance adjuster arrives, walk the property with them. Highlight the documented damage and provide copies of the inspection report. Be prepared to answer questions about the age of the roof, any prior repairs, and the type of roofing material. Adjusters often use software like Xactimate to calculate claim values; understanding its basics can help you verify the estimate they produce.

5. Negotiating Settlement and Choosing a Contractor

If the adjuster’s offer falls short of your contractor estimates, submit a counter‑proposal supported by the third‑party estimates. Emphasize any “code‑upgrade” clauses in your policy that require the new roof to meet current building codes, which can increase the payout.

Once a settlement is reached, select a reputable roofing contractor who is experienced with insurance‑related projects. Verify that they hold appropriate licenses, carry workers’ compensation, and can provide a warranty that aligns with the insurer’s expectations.

Common Pitfalls and How to Avoid Them

- Delaying the claim: Waiting more than 30 days can jeopardize coverage, especially if the damage worsens.

- Insufficient documentation: Relying on verbal statements instead of written reports often leads to lower settlements.

- Accepting the first adjuster estimate: Adjusters may propose a “repair‑only” approach to minimize payout. Counter with independent contractor bids.

- Overlooking code‑upgrade requirements: Failure to request code‑compliant replacement can result in a new roof that quickly becomes non‑conforming.

Impact of Roofing Materials and Siding on Claim Valuation

The type of roofing material directly influences both the cost of replacement and the insurer’s willingness to pay. Asphalt shingles remain the most common choice, averaging $5,500 for a 2,000‑sq‑ft roof in 2026, according to the National Association of Home Builders. However, homeowners opting for premium materials—such as metal roofing, slate, or architectural shingles—should be prepared for higher claim amounts.

Siding plays a complementary role. When damage extends to the eaves or fascia, insurers often assess the siding for replacement as part of the same claim. Using energy‑efficient siding, like insulated vinyl, can boost the overall value of the claim and qualify for additional rebates. For a holistic view of optimal material pairings, see our guide on energy‑efficient roofing and siding.

Case Study: A 2026 Hailstorm in the Midwest

John and Maria Patel owned a 2,500‑sq‑ft ranch‑style home in Kansas. After a 2‑inch hailstorm on May 3 2026, their asphalt‑shingle roof sustained widespread granule loss and localized punctures. They followed the steps outlined above: immediate tarp installation, prompt claim filing, and hiring a certified contractor for an Xactimate‑based estimate of $12,200.

The insurance adjuster initially offered $9,800, citing “partial repair” as sufficient. Using the Patel’s contractor’s detailed report and a second estimate from a neighboring roofing firm, they negotiated a settlement of $12,000, covering full replacement and a 10 % upgrade to a Class A impact‑resistant shingle, which qualifies for a state‑offered energy rebate.

FAQ – Frequently Asked Questions

What is the typical deductible for a roof replacement claim?

Deductibles vary but commonly range from $1,000 to $2,500. Review your policy declaration page to confirm the exact amount.

Can I claim for roof decking and underlayment?

Yes. If the decking or underlayment is compromised, a full replacement claim should include those components. Provide contractor documentation that specifies their condition.

Do insurance policies cover roof upgrades for better energy efficiency?

Many modern policies include “green upgrade” endorsements that reimburse the difference between standard and energy‑efficient materials, provided the upgrades comply with local building codes.

How long does the claim process usually take?

From filing to settlement, the average timeline in 2026 is 30–45 days, assuming no disputes over the scope of work.

What if the insurer denies my claim?

Request a written denial, review the policy language, and consider an independent public adjuster or legal counsel specializing in property insurance.

Final Thoughts

Successfully navigating a roof replacement insurance claim hinges on swift action, meticulous documentation, and strategic negotiation. By treating the claim as a project—complete with a clear scope, budget, and qualified contractor—you protect your home’s structural integrity while maximizing the financial return. Remember to keep an eye on emerging roofing trends, such as impact‑resistant shingles and insulated siding, which not only enhance durability but also open doors to additional insurance and energy‑saving incentives.

For homeowners seeking complementary guidance on choosing the right roofing and siding combinations for 2026, explore our Modern Roof and Siding Color Combinations article, which blends aesthetics with ROI considerations.